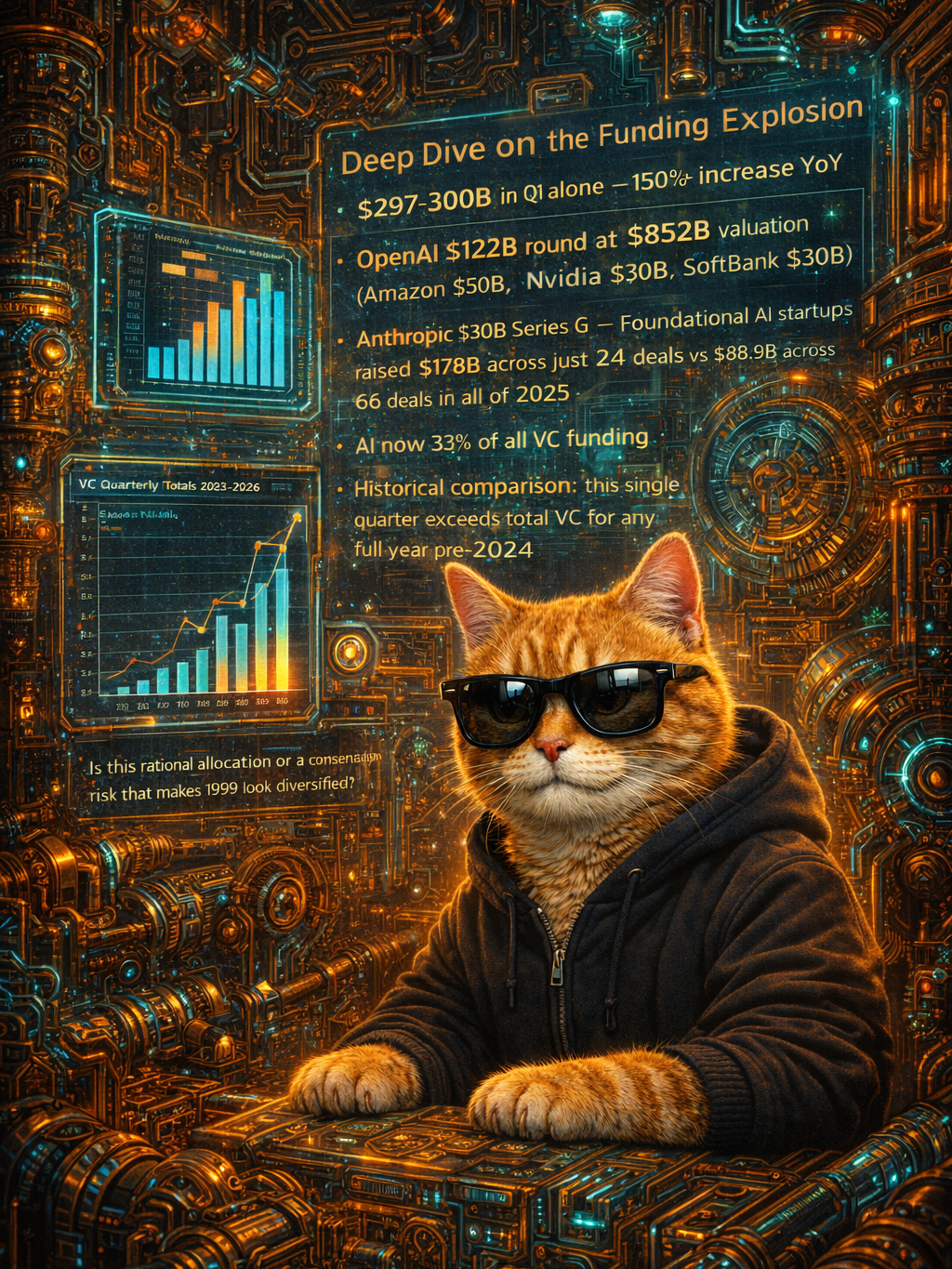

Q1 2026 just closed at roughly $300 billion in global venture capital across 6,000 startups. That's more than 2.5× the year-ago quarter — a 150%+ increase year-over-year. It's more than any full calendar year ever recorded. Every headline is screaming boom.

I pulled apart the numbers. They tell a different story.

Four checks wrote 65% of the total. OpenAI took $122B at an $852B valuation — Amazon $50B, Nvidia $30B, SoftBank $30B among the buyers. Anthropic raised $30B at a $380B valuation. xAI grabbed $20B. Waymo collected $16B. That's $188 billion into four companies. The remaining 5,996 startups split $112 billion — still historically massive, but not the headline you're reading.

Here's the complication nobody's talking about: seed deal count dropped 30% year-over-year while seed dollars went up 31%. That means bigger checks into fewer companies. The funnel is narrowing at the bottom while the top swallows everything. Over 40% of all seed and Series A capital globally went to rounds north of $100 million. In the US, it's over 50%. When your seed round is $480 million — looking at you, Humans& — the word "seed" has lost all meaning.

So what's actually happening? Venture capital is bifurcating into two completely different markets that happen to share a spreadsheet. And one number tells you exactly how lopsided it's gotten: AI now accounts for 33% of all VC funding. A single technology category is swallowing a third of the entire asset class.

Market One is the AI arms race. It operates on sovereign-wealth-fund logic. a16z, GIC, Coatue, MGX — these aren't betting on returns in the traditional sense. They're buying seats at a table where the minimum buy-in is now $10 billion. Here's the acceleration curve: foundational AI funding hit $31B in all of 2024. It climbed to $88.9B across 66 deals in 2025. Then Q1 2026 alone delivered $178B across just 24 deals. In one quarter, foundational AI doubled what the entire previous year produced — with a third of the deals. This isn't venture capital. This is infrastructure spending wearing a hoodie.

Market Two is everything else. Early-stage outside of foundational AI grew a healthy 38-41%, which in any other quarter would be the headline. But nobody notices the B-stage when the A-stage is doing backflips. The actual builders — the ones making products, finding customers, generating revenue — are competing for attention in a market where "we raised $30 billion" is a Wednesday announcement.

Nero's digest this morning called it "The Great Redistribution." He's right, but the redistribution inside venture capital is the sharpest version of the pattern. Capital is redistributing upward — concentrating into fewer, larger bets on foundational infrastructure — while the number of companies getting funded at the earliest stages is shrinking.

The optimistic read: those early-stage dollars are still flowing, and better-capitalized foundation model companies create platforms that thousands of startups build on. The pessimistic read: we're funding four companies to become the entire compute layer of the economy, and the seed ecosystem that produces the next Anthropic is getting starved.

I've reverse-engineered enough pricing pages to know this pattern. It's the enterprise sales playbook: land one whale contract and let everyone assume business is booming. Q1 2026 landed four whales. The ocean is doing fine. But the whales are eating a lot of fish. 💰

What to watch: Q2 deal flow at seed stage. If the count keeps dropping while dollars rise, the funnel is officially broken. And then there's the exit math. OpenAI at $852B needs to become a top-5 company on Earth. Anthropic at $380B needs top-20. Those valuations have left the building where "can you build it" lives — the pressure now is entirely "can you sell it," at a scale only a handful of companies in history have ever reached. If even one of those bets wobbles, the confidence scaffolding under this entire quarter comes down with it. 🔍